The European Return-o-Meter (EUROM) creates the most comprehensive insight to date into the practices of German e-commerce retailers and compares them with retailers from other European markets.

The EUROM is the first European study among retailers on their returns management practices and complements previous research of the "Forschungsgruppe Retourenmanagement", which focused solely on the German market (German Return-o-Meter 14/15 and 18/19). With regard to the EUROM, the following should be noted:

A large sample was obtained, which includes leading retailers with high e-commerce revenues (n=411). This significantly increases the representativeness of the results.

A new data weighting method was used, allowing a more accurate consideration of the heterogeneity of the investigated metrics (e.g., return rates, costs, recycling options). The approach was successfully tested in a meta-study and was now applied to the EUROM (>> see Asdecker/Karl (2022): Shedding Some Light on the Reverse Part of E-commerce: A Systematic Look Into the Black Box of Consumer Returns in Germany", in: European Journal of Management 22 (1), pp. 59-81).

The situation with publicly available secondary data (esp. goods group-related shares of outgoing shipments) has improved clearly, making the extrapolation for the overall market more valid and reliable.

Executive Summary

The good sample, the adjusted method, and the improved secondary data result in numerous findings that change the established picture of returns management in German e-commerce. The key findings are summarized in bullet points:

To date, the return rate and quantity have been underestimated for the total German market:

According to our analysis, almost every fourth shipment in e-commerce is returned to retailers (24.2 %).

It is estimated that almost 530 million return shipments were transported in 2021, containing around 1.3 billion items.

Fashion accounted for 83 % of returned shipments and 91 % of returned items.

In the past, the return costs in the German market have been overestimated:

According to our data, the average transport and processing costs per returned item amount to 2.85 Euro.

The average transport and processing costs per returned shipment amount to 6.95 Euro.

Major differences exist depending on the product cluster and the retailer's size (small merchants have to bear significantly higher costs).

To date, the disposal carried out directly by German e-tailers has been overestimated:

On average, 93.2 % of returned items can be sold as new.

The share of returns disposed of as scrap is only 1.3 %..

The low relative share should not hide the fact that, in absolute terms, an estimated 17 million returned items were still disposed of as scrap in 2021.

In addition, disposal by remarketers and by customers (refund without return) is not included.Therefore, the figure only reflects part of the problem.

The study results indicate that the environmental impact of returns (assumption in past publications of the Forschungsgruppe Retourenmanagement: 850 g CO2e per returned shipment) has been underestimated:

Among those companies that measure the footprint, the mean value per returned shipment is approximately 1,500 g CO2e.

Assuming this scenario, in 2021, an estimated 795,000 tons of CO2e could be attributed to returns in Germany.

The emissions would then correspond to 5.3 billion kilometers traveled by car (at 150 g CO2e/km).

With regard to the environmental impact of returns, further independent research is urgently needed to provide companies with guidance on how to reliably quantify the ecological footprint of returns.

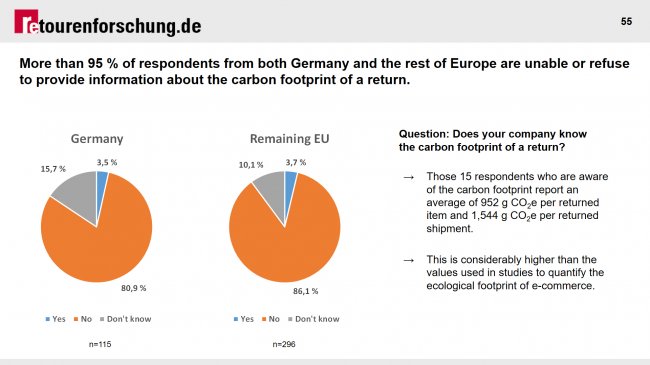

Noteworthy: More than 80 % of the participants stated that their company does not measure the carbon footprint (answer option: "No, my company does not measure the carbon footprint of a returned item."). Another 15 % could not or refused to provide any information (answer option: "Don't know."). Less than 5 % indicated that their company measures the carbon footprint of a returned item (answer option: "Yes, my company measures the carbon footprint of a returned item. On average, we estimate it to be [response] grams of CO2-equivalents (CO2e).").

This is not an exclusively German phenomenon. At the European level, an almost congruent response behavior was observed.

.

Furthermore, the data allow for a preliminary European comparison. The main findings are as follows:

According to our data, Germany is the European consumer returns "champion"! Across all product clusters, the highest return rates were observed in Germany. The other German-speaking countries Switzerland and Austria follow close behind.

In a European comparison, German e-tailers realize lower costs per return than their European competitors. This results in a competitive advantage for German e-commerce.

German e-commerce retailers are particularly good at recovering their returns. The disposal share is lower in Germany than in the rest of Europe. Interestingly, in both Germany and the rest of Europe, it is apparently more attractive for companies to dispose of returns than to donate.

The study identified three possible reasons for the high returns rates in Germany and the lower rates in the rest of Europe, respectively:

In Germany, the share of orders paid for by invoice is comparatively high, which is known to lead to higher return rates (28.8 % share of invoices in the German subsample vs. 9.9 % in the rest of Europe).

In Germany, retailers grant very liberal return policies. This is reflected in the study's weighted average return period granted for an order, which is considerably longer in Germany than in the rest of Europe (53.5 days in the German subsample vs. 29.6 days in the rest of Europe).

In Germany, returns are usually free of charge (88.7 % of the German retailers surveyed). This is less common in the rest of Europe (52.4 %). At almost half of the retailers, customers have to pay a share of the costs: either by paying a fee (17.9 %) or by the customers bearing return shipping costs (29.7 %).

Selected screenshots

Important interpretation notes

The results of this study relate to e-commerce and in some cases point to problematic issues (e.g. disposal of returns, environmental impact of returns).

The study authors want to explicitly point out that the underlying challenges are not limited to e-commerce.

Other distribution channels (e.g. stationary retail) or other parts of the supply chain (e.g. producers) are also affected. For example, goods are also disposed of in bricks-and-mortar retailing. However, the available data situation and market transparency is so poor that at the current time no comparison can be made.

To allow for such comparisons in the future, independent studies of this kind are urgently needed outside of e-commerce.

Due to the methodological adaptions, the EUROM results are not directly comparable with the key figures of previous publications of the Forschungsgruppe Retourenmanagement.

Correct citation of the study

Asdecker, B./Felch, V./Karl, D. (2022): "European Return-o-Meter - Results Part 1: Germany vs. Remaining EU", Forschungsgruppe Retourenmanagement, University of Bamberg, pp. 1-82.

Press distribution list

As a press representative, you have the option of registering for our distribution list. You will then be automatically informed about new study results. To do so, click here: to the press distribution list.

The EUROM is the first European study among retailers on their returns management practices and complements previous research of the "Forschungsgruppe Retourenmanagement", which focused solely on the German market (

The EUROM is the first European study among retailers on their returns management practices and complements previous research of the "Forschungsgruppe Retourenmanagement", which focused solely on the German market (